Many assume that scammers just target the more mature in age, but they go after everyone. Younger people who may have been manipulated may not have the same amount of money to lose, but that doesn’t mean they aren’t being targeted.

Today’s guest is Kathy Stokes. Kathy is the Director of Fraud Prevention Programs with AARP. She leads the AARP social mission work to educate older adults on the risks that fraud represents to their financial security. She currently serves on the advisory council to the Board of International Association of Financial Crimes Investigators and on the advisory council to the Senior Issues Committee of the North American Securities Administrators Association.

“Now I’m talking to workers who are retired and telling them that all the great stuff they did to ensure they could live through retirement is at risk.” - Kathy Stokes Share on XShow Notes:

- [1:02] – Kathy shares her background, what she does at AARP, and what AARP actually is.

- [3:50] – AARP has had a Fraud Watch Network for a while, but its current form is different from years past.

- [5:29] – There is a concerted effort to bring the generations together to educate others in the community.

- [7:26] – It is a common misconception that older people are targeted more often than other age groups.

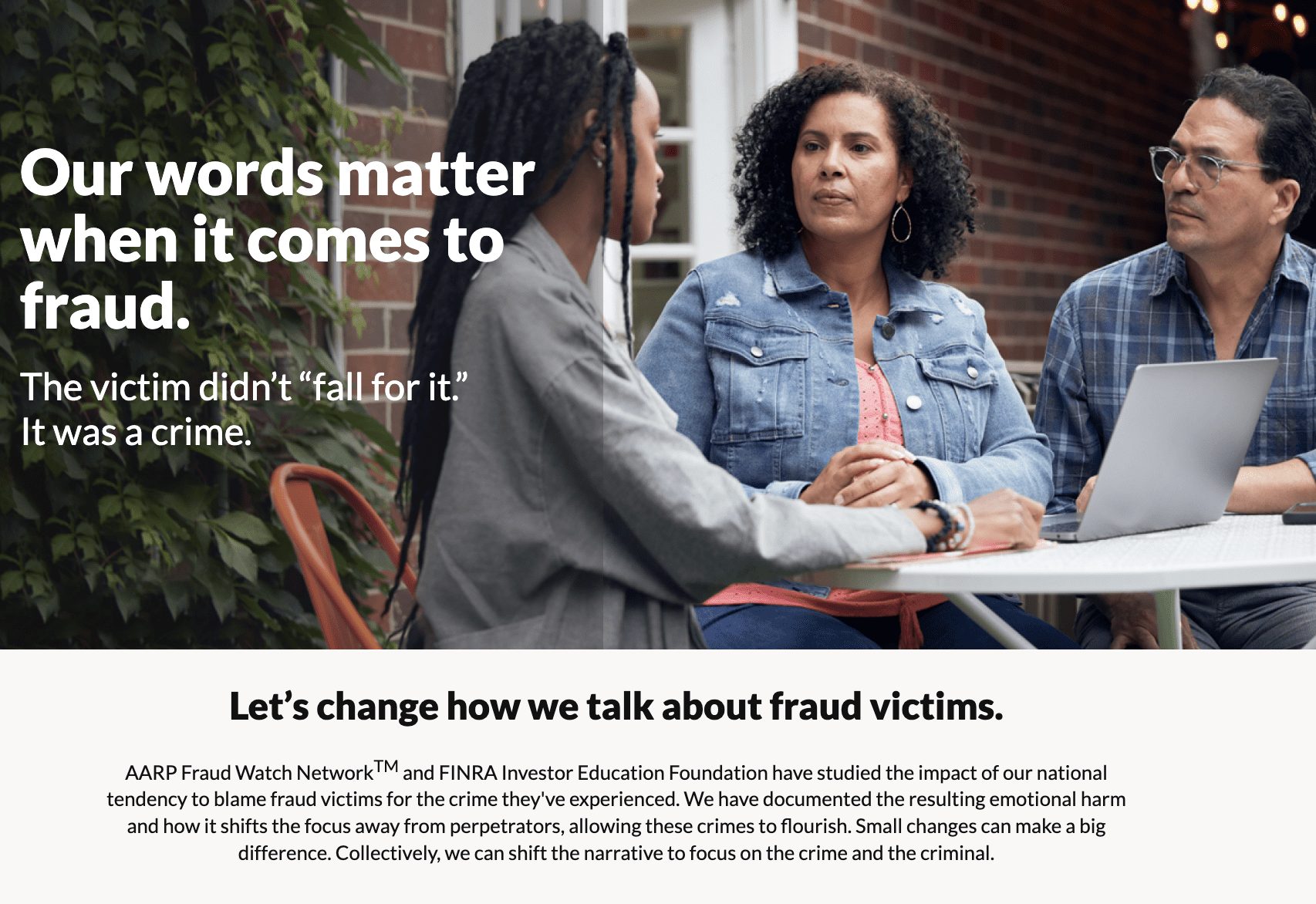

- [10:38] – The biggest barrier is something that is beginning to break down. It’s the shame and victim blaming. We are at a turning point.

- [12:50] – Unfortunately, police officers are not able to do much for financial crimes, but it is still important to report them.

- [16:01] – Most scams are considered “low ticket” items, even if it is several thousand dollars and that’s all you have.

- [18:08] – AARP has a resource for how to talk about scams with family members who have been a victim of a scam. https://www.aarp.org/saythis

- [20:50] – Rewording how we talk to and about victims of scams is changing.

- [24:23] – You have to have a strong and unique password for literally everything.

- [25:27] – Even just one extra layer of protection in the form of two-factor authentication is helpful.

- [28:10] – No one will ever ask you for an authentication code over the phone.

- [30:20] – There’s got to be something we can do as a society to help victims with the money they’ve lost.

- [32:48] – We cannot trust incoming communication, including calls, emails, and texts.

- [36:45] – Education and continuing to talk about this will help keep the trend of less victim shaming going.

- [39:30] – Victims can change the verbiage as well. Report the scam and file a police report.

- [41:29] – You can and should also report scams you know about even if you did not experience a loss.

- [43:10] – A number to use to reach the Fraud Watch Network is 877-908-3360.

- [48:09] – If someone you know has been a victim of a scam, don’t get mad at them for “falling for it,” get mad that this was done to them.

Thanks for joining us on Easy Prey. Be sure to subscribe to our podcast on iTunes and leave a nice review.

Links and Resources:

- Podcast Web Page

- Facebook Page

- whatismyipaddress.com

- Easy Prey on Instagram

- Easy Prey on Twitter

- Easy Prey on LinkedIn

- Easy Prey on YouTube

- Easy Prey on Pinterest

- AARP: Say This

- Fraud Watch Network

Transcript:

Kathy, thank you so much for coming on the podcast today.

I'm so glad to talk to you today, Chris. Thanks for inviting me.

You're welcome. Can you give myself and the audience a little bit of background about who you are and what you do?

I work for AARP. AARP is a confusing organization, even from the inside, so I like to explain that AARP is in three parts. There's the for-profit, AARP Services Incorporated. Those are all the folks that are working on the daily to try to get really great discounts and membership resources for the 37 or 38 million people who call themselves AARP members.

We also have a foundation that works on the charitable angle of the work that we do to support older adults. Then there's the social mission stuff that's in between—we call it the enterprise. Within that, that's where all of our education and outreach work happens, our advocacy work, things like that.

I run a program called the AARP Fraud Watch Network, and we're all about helping older adults—really everybody—understand the significant risk their finances face because of the threat of fraud that has just grown exponentially over the last five years. We do a lot in the space of supporting people who've experienced fraud.

That's great. Was there something in particular that got you into this field? Does it want to tap you on the shoulders and say, “Hey, I think you'd be great doing this”?

It sounds like it was meant to be if I look back at my career in a certain lens. It wasn't as exact as this, but in my early career, I was doing government affairs and public policy around issues of the move from traditional pension plans to the do-it-yourself 401(K) and what that meant to future retirement security.

I went from a public policy angle to actually doing financial education for large employers for their employees for many years, helping them understand the benefits of the 401(K) and all that stuff. I had my own business for a decade—communication, consulting—but a lot of it was around this employer benefits for the 401(K) and stuff.

My career has moved from educating current workers about how to save, invest, and be prepared for a financially secure retirement, and now I'm talking to those workers who are now retired and saying, “All that great stuff you did, to have all these assets, to have you be able to live through retirement, are at risk.” We've got to talk about how to protect ourselves and what we need to be doing as a society to really address this paradigm shift.

When did AARP start their fraud prevention programs?

It's actually been around for a long time, but not in its current form. We have offices all around the country, and probably four or five offices have come together. They were across the country not even geographically close, but they all had this idea that we're seeing a lot of this happening out there. We're talking like in the mid-2000s. We should do something about it.

They created their own Fraud Watch Network programs. They had staff devoted to it. They trained volunteers. AARP has probably 40,000 volunteers around the country, and the ones that sign up as volunteer fraud fighters go out into the community. They were doing great work, and at some point caught the attention of AARP's National Office, and they created a nationwide program. I'm going to say that might have been around 2013.

Then in 2019, we revamped it, moved it from one part of the organization to the other, and brought a lot more resources toward it. The new Fraud Watch Network has been around since 2019.

Do you find that the communications coming from that department and the team are more accepted by older Americans? I know when you have, let’s say, people that are 20-something going into a senior community and are, “Hey, we're going to do a presentation on fraud,” they're like, “Ah, you kids. I don't want to listen to you.”

We actually see a nice comfort level with that intergenerational conversation. But the reality is most of our volunteers that go out into the community are older because they're retired. Now they're in a place where they want to get back. But we also do a lot and some at specific states where there is a concerted effort to bring the generations together so that they can learn from each other in a variety of things.

Definitely, technology is one of those things that has always seemed to younger generations to be more on the cutting edge of technology. Older generations are a little less comfortable with that new technology.

I would say it's less about the generation's comfort level and more around the technology industry focusing on the younger adults who are more adaptive when new technology comes out. They're missing a really big part of the market where they're only appealing to people that are their own age—20s and 30s—instead of people like me and my mom—50s and over—who I'm great with technology that I know. But when the new stuff comes out, it's not because I don't understand it because I'm older. It's because it's not geared to me. It's geared to a 20-year-old.

I'm great with technology that I know. But when the new stuff comes out, it's not because I don't understand it because I'm older. It's because it's not geared to me. It's geared to a 20-year-old. -Kathy Stokes Share on XSometimes it's just a matter of familiarity for the longest time. I was an iPhone person, my wife was an Android person because that's what her company gave her. Anytime that she needed tech support on her phone, I'm like, “I can't help you because I don't know anything about this platform.”

Perfect analogy.

“It was just easier if you switch to iPhone. Then I can help you.”

Did she?

Yes, she did, actually.

Nothing against Android. They're going to be on the same platform to help each other.

It's very much a preference issue and what you're used to. When you're in someone's ecosystem, it's sometimes hard to switch to a different ecosystem.

Does AARP see that? I think the conventional perspective is that older people are more targeted by scammers and fraudsters and criminals. Do you guys see that as the case or is it just that's the narrative we like to use?

We really don't know how much fraud is out there because you have to report it for anybody to know, and it's severely underreported because of victim blaming and shame and all this stuff. -Kathy Stokes Share on XI am so glad you asked that, Chris. We really don't know how much fraud is out there because you have to report it for anybody to know, and it's severely underreported because of victim blaming and shame and all this stuff. But even at what we know, the Federal Trade Commission has been looking at this data for many, many years, and they have always seen that more younger adults when they report a fraud or scam to the Federal Trade Commission, they lose money more often than older adults report.

It's always been there. It's just when that older adult is the target, there's so much more potential loss. And it makes sense. If you're 23 or 24 years old, just out of college, and you're at the beginning of your career, you don't have a lot of assets. They are tied up in other things. You're at the bottom of your earning ladder.

When you're 80, you've been retired, and you're not going back into the workforce, and all that money gets stolen by these criminals who are increasingly sophisticated, what is that person to do?

Also, I think if a 20-year-old has their bank account taken over and $1000 gets taken out, all the money that was in their account, “OK, that's fine. I can recover that $1000 over the course of the next month or months.” But if you're in retirement and someone takes over an account with $100,000 and takes all of that, this person's been retired. Aside from victim services or the criminal justice system, they're not going to be able to re-earn that money.

That's exactly the point. Even for the 20-year-old who loses the $1000—well I should say not loses, stolen from them—that’s terrible. It shouldn't happen. Like you said, there's a time horizon where they can make up for that. That's just not the case when you're on the other end of the age spectrum.

Every time I talk to somebody who's providing support services, the discussion of reporting always comes up. Whenever we talk about the $10 billion a year, $40 billion a year, everyone says it's significantly underreported. What are some of the biggest barriers to people reporting fraud and theft in this community?

I believe the biggest barrier is something that is actually beginning to break down. It's the shame, the victim blaming. I think that we're almost at a turning point and we can see it in our own research where three or four years ago, even if I were to say, “Chris, do you think you would ever fall for a scam?” And you'd be like, “Not me. It's not.”

When somebody would fall for a scam, you're probably automatically going to, “OK, what was it about that person that made them gullible or vulnerable? Do they not know tech? Are they older, so maybe there's cognitive decline?”

That has been a very active part of the narrative. We've deprioritized fraud as a result. Because if you can just say it only happens to older people, you have cognitive decline, and it would never happen to me, we don't have to worry about it. But we're beginning to see that change.

Just last week, maybe it was two weeks ago, we launched new research where we ask people about their concerns about fraud. We're not hearing, “That only happens to somebody else.” Ninety-one percent of US adults worry about fraud now, and their number-one concern is becoming a victim themselves. That begins to allow for that change that we need to see.

Ninety-one percent of US adults worry about fraud now, and their number-one concern is becoming a victim themselves. That begins to allow for that change that we need to see. -Kathy Stokes Share on XI think there is a perception difference about it when you hear someone being targeted on the basis of something like a financial crime. We often do think, “What did they do wrong? What did the person do wrong?” We don't say that when the person walks down the street and gets mugged or they get carjacked. You're not like, “Gee, if they just walked down the other side of the street, they would have been fine.” We don't talk about it that way.

Maybe sometimes we do a little bit, like, “Did they lock the doors?” But it's a small part of the larger discussion. That person is still seen as a crime victim. Police show up, possibly investigate, and they find the bad guys who go to prison. That is not really happening in financial crimes.

Are you starting to see that increase as far as the police getting involved and actually doing investigations? I think the impression a lot of people have is that the police will be, “Sorry, that's a financial crime. We can't do anything to help you. Have a nice day.” And that's it. Is that really what's happening on the ground? Or does it really vary from place to place?

It certainly varies, but that is the theme, unfortunately. It is no fault of the police officer who answers that phone when a victim calls. It's not a priority. They're made to believe, or they believe, for whatever reason, that property crimes and violent crimes are the things they can do something about. When it comes to financial crimes, it's like, “Ah, well, you gave them your money.”

There are a lot of financial crimes investigators around this country that are detectives or are working in private business who really get it, and they will go after it and try to help the victim. But by and large right now, we don't have.

What I still try to tell people is report the crime for two reasons. One is the more we're reporting, the more societally, we understand that this is a problem that we have to address as a whole of society. The other thing is what happens if two or three years down the road, your state legislature or even the federal government—although we know they don't do a lot these days—might create some restitution fund for financial crimes victims, and what better way to appeal for that support but with a police report?

Or someone else might have reported the same person and then as part of that investigation, they do recover money. It would be nice for you to get part of your money back also.

Exactly right.

I know that you're not in law enforcement here, so if you don't know, that's fine. When these are investigated, are we starting to see more of them or a larger percentage of them result in arrests and convictions?

I think the big challenge is that there are investigations that happen. There are investigations that never stop, start to begin with because the US attorney doesn't want to deal with it or doesn't understand the impact they could have if they did prosecute. A lot of this is driven by crime rings that are outside of the country, and there's a presumption that you can't get the bad guys anyway.

But when someone just pulls a thread that begins to unravel some things, you do get to see that there are tons of people, of aiders and abettors in the United States, working as money mules, money launderers, guys who pick up the money and send it to the next place or go into the bank and cash the fake check and get some dollars out of it. It's going after those.

The problem is, these scams that are happening are in terms of law enforcement—I'm thinking specifically federal law enforcement—they're low dollar. Even if it's a $10,000 scam and that was everything you had, it's not a low dollar to you, but unfortunately it is because of resource-constrained federal law enforcement.

But if there was a way to connect that $10,000 loss that was related to someone pretending to be your grandkid and connected it to the $8000 here and the $9000 there and the $12,000 all around the country, and all of a sudden you have an investigatable case because you've hit a threshold and maybe with the FBI, it's $1 million. Take enough of those $10,000 cases, put them together, be able to tie them back to the same MO, and be able to actually hand that off to the FBI to go out and arrest people. You begin to disrupt the fraud business model.

In my mind, that seems to be a parallel to how we've handled drug crimes. If you go after the middleman, it just makes it harder for the people outside of the country to perpetrate the crimes if the middlemen aren't available to do it.

The point is to get them off the streets and get them real time. There was a case that they actually did it this way in San Diego County a bunch of years ago, and they ended up taking down the US end of a grandparent scam ring where people had millions of dollars stolen from them.

They get arrested, they go for prosecution, and the judge gets it because the lawyer for the purpose is like, “He was just moving money from point A to point B.” She's like, “You are a vile human,” and gave him nine years. Not just a slap on the wrist and back out tomorrow.

And hope they don't get out for good behavior because they didn't commit any financial crimes while they were away from the Internet.

We hear of financial crimes that happen within the walls of prisons, too.

Anywhere the technology can eventually get, it'll happen. What are some of the things that we can do around reducing the blame and shame aspect of it?

I have a website that I would love folks to go and visit. It's aarp.org/saythis and it's directed to a concert audience. We're thinking mostly of those adults who have older loved ones that they provide some form of caregiving to, to help them understand that if a fraud like this happens to their aging mom or dad, to understand it's […]. It's not something they did wrong.

Even short of that, we need to be talking about scams that are out there regularly. We have a national dialogue. More people know what the scams are and can see them coming.

There was research done by the FINRA Investor Education Foundation back in 2019 with the Better Business Bureau, I think, and they were able to determine that if you know about a specific scam, like the grandparent scam, you're 80% less likely to engage with it.

When we're talking with our moms and dads, aunts and uncles, even brothers and sisters—”Hey, I read about this scam the other day.” Or, “Someone just told me that they got an invite from their neighbor and it turned out that it had software in it that drained their bank account. What do you think about that?” Have the conversation because it really is protective.

Then it's about choosing the language and this site helps with that. We also have a professional version and that's aarp.org/wordsmatter for financial institutions, for helplines, things like that, law enforcement, and adult protective services understand the victim experience.

My mom didn't intend to wake up and send $10,000 to a criminal. She intended to help her grandson when she thought it was her sole ability to help him. Think about the context. Don't use the words that say like you were duped to say somebody stole money. We are starting to see a change.

What are some of the other language elements that we should be avoiding? Some of it, I don't think it's intentional from people, but it's how we've talked about these things in the past. But if we don't talk about them now in the way that we're using them that hurt people, we can't change that. What are some of the other phrases that we use that are not appropriate and that disincentivize people to report?

I think it's the focus on something that the victim did. The victim fell for it. She was scammed out of $1000. Duped, swindled, tricked, those kinds of things don't even bring into the discussion that there was a crime committed, that there was a criminal perpetrator. We try to just rework the sentence. A criminal stole this woman's life savings. There are a bunch of examples on our site that I referred to before that helped to get to that.

We even see it in media coverage and, fortunately, we are seeing a lot more media coverage of the scams that are happening and that's helping to educate people and know what to look for. But we ran into the Vermont woman duped $50,000. Older lady was scammed, she's so embarrassed. Instead of this criminal intentionally targeted this person and that person now has nothing.

You don't say the bank teller was duped into turning over $10,000 out of her cash drawer when the armed robber came in.

You know what? Anytime there's an armed robbery of a bank, it's investigated 100% of the time. The money is typically found and returned, and if it's not, it's insured. Not quite the same when it's an individual.

That is really challenging. I see the perspective of the news and, unfortunately, news has gotten very much about eyeballs and clicks. We want to say things that are sensational to attract attention, but that doesn't really help the people involved to do it that way.

I think that the same reporter that used to write about a Vermont woman duped of life savings would see the value in focusing on the criminal. I don't know if sensational is the right word, but it gets attention. There's this bad guy out there who's preying on everybody they can get their hands on. They're wiping them out and there's no recourse.

Criminal steals money from a 110th victim this week.

Yeah. We’ve got to get you into the reporting business.

I'm trying, and this is definitely for me having run the podcast for four years, having to change the language that I use because more and more people like you and other guests have said, “Hey, that's not a good way to look at this. That's not good phrasing to use.” I think none of us are in a position where we can't learn to help victims better and communicate with them in a more effective way.

I think what your bottom line is, Chris, is there are things each of us can do. There are steps we can take. I have a mentor in this field who refers to it as hardening the target. Like when you go to bed at night, you lock your doors and windows; you lock your car when you walk away from it. These are those kinds of things.

It's just a matter of getting the word out to enough people so that they understand that there are things they can do, and that's a real challenge for educators. Some of those things are like passwords. We're really bad at passwords, and we really shouldn't be blaming ourselves. It's a system we inherited, but it's inherently flawed because you need a strong and unique password for every single online account. How many online accounts do you think you have?

I'm guessing I probably have at least 200.

And you have to have a strong and unique password for 200. Even if it's just like your son's baseball team's list that you have and all up to your financial accounts because if either one of them is similar or the same and one gets broken, the other's broken as well, and there are ways to monetize even non-financial accounts.

We try to talk to people about how to create strong and unique passwords and the importance of it. But also if you're comfortable in the space of using a password manager, consider that. If you're not, and you have, like I do, an iPhone where I can put a note in my phone for my usernames and passwords, but then I encrypt that note, and my phone itself is encrypted, so nobody can just pick it up and open it, that's the way.

Multi-factor authentication is so important. It's not foolproof, but if you have that extra layer, that one more piece of information that authenticates that it's you trying to access your account, that helps us a lot.

Obviously, I talked to cybersecurity people who will have their views on SMS. “Oh my gosh, it's utterly useless. It's a horrible form of two-factor authentication.” I disagree with that in a sense. Do you find older adults have a harder time with the different elements that you can use for two-factor authentication, whether it's an SMS, whether it's a physical key or a physical thing that they have to look at or an app that stores the […].

I don't know that we actually have research on that per se, but we do have a lot of research on technology used by older adults. It's a lot more pervasive in a good way than you think of people that can use technology and use it well and understand how to interact with it. I don't really think it's an issue there, but true. If you get a text message with that code and someone is socially engineering you to believe that they're the bank and they're sending you that code, it's bad. But it's something.

I just recently had a friend tell me that story that he got a call from what he thought was his bank saying, “Someone has accessed your account and you need to make a change to your account.” “I just need to verify that you are the person claiming to be the bank.” “I need you to verify that you are the customer.” “I'm going to send you a one-time code. If you read that back to me, then I can confirm that you're the customer.” He did it and then he was like, “Oh no. This is probably not my bank,” so he immediately hung up, called the bank, got to change everything and all that.

Luckily, no one got into the account, but it got me looking at my own SMS two-factor authentication messages. Maybe only a quarter of them say, “We will never ask you for this over the phone as part of the token.” It's usually just, “Here's your six-digit code and it expires in 30 minutes,” rather than saying, “We will never ask you for this code. If someone is asking you for the code, hang up the phone.”

It is so important to have that piece of information associated with the number, with MFA, and not even because if I'm thinking that someone is actively taking money out of my account, I may not even read that. I may just use that number. But if I'm not in that situation and I see that regularly, which I do with more of my accounts then not now, it's a great reminder for me so that if someone were ever to ask me, I would be like, “Wait a minute. That's out of the norm. I'm told not to.” I think there's a really important preventive educational element to that as well as […]

A little bit of standardization needs to happen at the financial institutions. Are you finding that financial institutions are now being more responsive when fraud and scams happen?

I think that a lot is going on here. They are specifically talking with financial institutions that I work with. For example, I'm on a federal reserve working group with financial institutions on scam information sharing, a really tough nut to crack, but there's a lot of focus and a lot more on understanding that this person is a victim of a crime, and they deserve our empathy, our support, and whatever we can do within our abilities to try to claw back funds if they haven't received yet or haven't left the account yet.

I see a lot more focus on that, but at the same time, I think a lot of people would look at financial institutions and say, “Look, that person's account just got wiped out through social engineering. No fault of theirs, understandably not a fault of yours either, perhaps. But that's everything that person had. You should just cover it.”

But that brings up so many more issues of moral hazard and people knowing to game the system. There's got to be something that we as a society can do to address these losses.

You mentioned at the top, like maybe $10 billion a year. I would point into a Federal Trade Commission study from October of 2023 when they were talking about how underreported fraud is. In it, they talk of an extrapolation they did. This was on 2022 data so then it was like $9 million. Based on underreporting, their extrapolation gets us to $137 billion in losses in 2022.

It's about one out of six gets reported then?

The way they looked at it is if you had under $1000 stolen, you're probably about 2% of that is reported, whereas if it's over $1000, maybe it's 6% or 7%. So yeah, right in that window, $137 billion.

I totally understand that under $1000, people wouldn't report it. The phrase I would use for myself, and I'm not saying that other people should necessarily think of it the same way as I would think it was a tough lesson learned for myself, for me. It's not that if you have only $1000 in your bank account, that's not a tough lesson learned, that's a horrific circumstance in your life to face. But I think there is that perception of smaller amounts are definitely going to get reported less frequently than the larger amounts.

Yeah, but you make a really good point because $1000 means very different things depending on where you sit.

Yeah, it's relative. If I'm in Africa making a dollar a day, $10 is a massive amount of money. If I'm independently wealthy, $1000 is dropped on the floor, it's not worth picking it up. People's circumstances significantly impact what they're going to do, or what people should do.

We talked about people using password managers. What are some other things people should do to protect themselves? The equivalent of locking your car door when you walk away from it, locking your front door, closing your windows at night, these sorts of things.

Unfortunately, where we are in society right now is we cannot trust incoming communications, that phone call that doesn't come from a list, like your daughter, your son, or your doctor, you have to let it go to voicemail, or if you have an answering machine. Let the technology on that side help weed some of this stuff out because the phone is still a huge broad vector.

So is email and increasingly so is text. When you get an email and it's from Amazon and you have an Amazon account and it says, “Hey, we just want to make sure that you made this purchase of seven iPhones for $12,000. If you didn't, you can ignore it, but if you did, click this link.” It looks like it's from Amazon and you're like, “Oh no. That wasn't mine.” But if you click that link, you're going to the criminal.

We have to try to learn that in an email or a text and it's coming from a retailer we do business with, a bank we do business with, don’t engage with it. If you have an Amazon account—97% of us probably do—instead of clicking that link or calling that number that they're providing, you have the app, log into the app. You are on the website, log into the website. If there's a problem, you'll see it, so we just cannot trust the links.

Social media is a huge risk vector right now for a variety of frauds. Someone hacks somebody's Facebook account and all of a sudden they're pretending to be that person and telling all of that person's friend group that they had just collected $12,000 in a federal grant and you can too; just click on this link. All of that stuff is happening very regularly, so we have to be cautious.

If we're on social media, we have to make sure that our accounts are locked down. They come to us completely open. I think they should come to us completely locked down and then we can opt out, like, “No, I don't want just my family to read what I'm putting on here,” or open it up and let everybody read it. But that needs to be a consumer's decision.

We've seen that concept work with savings for retirement. If people are opted in when they start with their job to save for retirement, 90% of people don't opt out of 401(K) contributions. But if the company doesn't automatically turn it on, it's like only 20% of people go in and say, “Yeah, I want to add to my retirement contribution.”

It's funny you brought that up because I worked on that project to try to get Congress to say it's OK for employers to do the opting in back in 2005 or 2006 at the working institution. That's very close to my heart and history.

We are starting to see some banking services starting to say two-factor authentication, when you set up your account, it's the default. It's not, “Hey, let's add some extra security. You have to go out of your way to reduce your security. We're going to give you lots of red screens that say you're increasing your risk by doing this,” as opposed to, “Hey, customer. We've got this big, nasty, long process to do that will increase your security.” Then they downplay it and talk about how horrible it is because people who want to sell you stuff don't want increased friction. They want decreased friction.

I think it would behoove all of us, no matter where we sit in this world, to recognize that friction is not a four-letter word. Friction is good sometimes and if we can explain to a consumer why we're doing X, Y, or Z to protect your account. There's going to be a lot more acceptance of that.

I love that phrase. Hopefully no one has trademarked it. Friction is not a four-letter word. It's funny because if you look at so much in our life, companies are spending millions and billions of dollars to figure out how to reduce friction, and the criminals with the scams are trying to do the same thing. If we add friction back to our life, we reduce the chance of being taken advantage of. Now I'm thinking of my wording here. Reduce the chance that someone is going to steal from us or target us.

Once someone has been targeted for a scam and they've lost money, what should they do? Who should they contact?

If it had anything to do with your bank account, financial institution, contact them as soon as you realize what happened because there may be an opportunity for them to stop a transaction or to at least stop some of the transaction.

If you were coerced into believing there was a huge financial emergency and the best way to solve it was to buy gift cards and share the information on the back of that card, as soon as you realize that that happened, flip that card over and call the number on the back.

Criminals are really good at this gift card payment stuff. It's not as big as crypto right now in terms of a payment form. There was a time at least where I was being told that the money wasn't being drained right away from those cards because they were just doing it so much, they didn't have time. The chances that you might get some of your money back by freezing the card by talking to the company that issued that card could help you.

And obviously report to local law enforcement.

I think the most important bottom line here is reporting it to law enforcement. We talked about the underreporting problem. A lot of valid reasons for it, but not good reasons. If we can disabuse this notion that it's our fault, we did something wrong and we're being stupid and we don't want anybody to know and instead get angry and say, “Look, somebody made me believe something that wasn't true. Now they've stolen X, Y, Z. I want a police report.”

Will the police actually execute an investigation? Not sure. Probably not at this stage, but that information may help them with other cases that they have, and it's certainly going to help you not hurt you if somewhere down the road there was a means of restitution. You have a report to prove what happened.

I think it parallels our health is that you have to be your own advocate. Don't just assume that the police are going to follow up on it. Don't just assume that the bank is going to do their part. This is what happened. What are you going to do? And what are you going to do about it?

Yeah, and I think people do want help. It's just that growing understanding that it isn't the fault of the victim is really helping the frontline responders to maybe approach their response to it differently, even if they're not able to recover funds. Maybe there are other ways that they can react to that person so that person feels validated that something bad happened and it wasn't their fault. It goes a long way.

Do AARP provide victim services?

We have a great program. My colleague, Amy Nofziger, has run our Fraud Watch Network Helpline since way before there was an official national fraud watch network. I told you about several states back in the early days.

It's gone through a lot of change now. She went from maybe a dozen trained volunteer fraud specialists taking calls to now over 200 around the country, and it's not a hotline. It's not like 24/7 but 8 AM to 8 PM Eastern, Monday through Friday, you call this number and I'll share it in a second.

If you're just reporting a scam because you don't want somebody else to experience it, but you didn't have a loss, we stop at level one. We say thank you and we record that and send it to the Federal Trade Commission. If you're not sure about something, if you've experienced fraud yourself or a loved one has or is in the freeze of it, go to that next level and it's these 200 fraud specialists and you actually get to talk to a human being.

Oh, that's good.

Last year, I think the incoming calls were around 97,000. Then we have a program that we stood up about three years ago, which is growing now. I'm so heartened to know that people are starting to learn about it through these online, small-group Zoom support sessions.

We have a trained facilitator and maybe five or six people who are willing to talk about what happened to them. Just get on the phone together on a Zoom call together. It's about supporting each other, understanding that it's not your fault, you're not alone, and really start looking at the negative emotional impact that so much of this causes.

It's about supporting each other, understanding that it's not your fault, you're not alone, and really start looking at the negative emotional impact that so much of this causes. -Kathy Stokes Share on XI think we thought it would be like a starting point for people and then they would move on and do whatever. We have repeat attendees all the time because it's so helpful for them to keep hearing, “Yes, I'm sorry that happened to you,” and to be able to take that in and give it.

What's the number for that?

The helpline is 877-908-3360. Then the online program you can learn more about and sign up at aarp.org/fraudwatch.

We'll make sure to include those in the show notes. As we start to wrap up here, what are you seeing as the king of the next big context around scams.

I think the biggest concern for me right now is fraud related to cryptocurrency. We're seeing two aspects of that. One where it's being used as a method of payment. When someone tries to make you believe there's an emergency and you've got to convert money at the bitcoin ATM down the street and send it off to solve whatever problem it is […].

The more concerning one is cryptocurrency investment schemes that start out with something as simple as what seems to be a text message sent to you in error. We're seeing so much of that and that message comes to you.

My example is always like, “Dr. Smith, Fluffy is really sick in a green room right now.” And who doesn't want to help Fluffy? Who doesn't want to help Fluffy's owner? So you respond and say, “I'm sorry about Fluffy. I'm not Dr. Smith. I hope everything works out.”

That begins the opening to a discussion, to a conversation that goes on to eventually building a trust relationship. This is weeks and months. Then that person, your new best friend on text, says, “Hey, I've shown you how high I'm living and it's because I invest in crypto, and I can teach you how to do it.” It is just wiping people out. Wiping people out.

Again, someone might be hearing that going, “How could anybody not see through that?” Well, you don't because the criminal has a playbook and the playbook is it plays out if the person engages with a seemingly errant text—that’s all it takes. It's not that big of a swell. I want to say that too.

I was surprised that there was a piece of time, maybe a couple of months ago, that I was getting one or two of those text messages a day to any one of the variety of numbers that I have for different things that it would be, “Hey, this is Michelle. I'm running late for my appointment. Can you let Bob know that I'm running late?” There's a sense of urgency there. It's trying to catch us with a sense of morality and doing the right thing and being a good person to help out.

The first one I got, I think I sent a response. I was like, OK, this is odd. Let me send a response. The person sent back a photo of themselves. Well, not them, but they sent back a photo. I'm like, “OK, no one I know would ever send a photo claiming to be of them to someone they don't know.” I'm like, “OK, this is a scam. This is the lead for the scam.” The beautiful young lady accidentally texted me and now wants a relationship. I don’t…. But it was, “OK, here we go. We're going down this road.”

That sounds to me like a scammer who hasn't gone through 101.

I've seen those things even on LinkedIn. “You have such an interesting background of work experience. Maybe we could be friends.” I'm like, “Mmm, that doesn't sound like a normal professional introduction on LinkedIn to me.”

Sometimes it's just accepting a LinkedIn request because that person is showing up in the LinkedIn world of people that you have relationships with or have respect for, so you're like, “Oh well, if he's in that guy's LinkedIn network then he can be in mine,” and it seems so innocuous.

But that's all it takes for that LinkedIn person to reach out to you and have conversations about the things you really care about because they're monitoring your LinkedIn to begin a relationship that goes the same route.

Oh, it's a scary world that we live in, that people have decided rather than working hard, they're going to try to steal money from people.

That's been since the beginning of civilization. Badly. But there's a message of empowerment too and it's being aware, it's sharing what you know, it's understanding that these are crimes, and the victims are victims. They deserve justice. They deserve empathy and respect.

If it happens to you, get mad about it, want to do something. If it happens to someone you love, don't get mad at them; it's not their fault. Get mad at the person, the people behind these schemes, and seek to do something. -Kathy… Share on XIf it happens to you, get mad about it, want to do something. If it happens to someone you love, don't get mad at them; it's not their fault. Get mad at the person, the people behind these schemes, and seek to do something. Bring justice somehow, in whatever small or big way. But we all have to be doing so much more in this space.

I love that as a great summary of our discussion here is to get angry and do something.

It's time. It's time, folks.

Don't do anything illegal, but do something.

Yes, and don't stay on the line with a scammer because you know it's a scammer and you think that they're just wasting their time. That is something people love to do. But the longer you're engaging with that scammer the hotter your number is or the hotter your text address is, whatever. They buy and sell these things. If you engage for a minute or more, you're getting so many more scam attempts, so disengage.

I love it. Are there any additional resources that you want to make sure we mention as we wrap up here?

I mentioned that the program I run is the Fraud Watch Network and we have a website for that, aarp.org/fraudwatchnetwork. There are lots of great articles on what's happening out there. We have a fraud resource center, tip sheets on the latest types of scams. We have a scam-tracking map. You can report a scam you've seen in the wild there.

We have a great podcast as well. Chris, I don't know if you're familiar. It's The Perfect Scam by AARP. We really take the focus of victim impact. The cunning criminals who are getting away with all this stuff. It's really the focus on, “OK, this is the after.”

I love it. We'll make sure that we link to all those resources. I think Adam does the […].

Currently it's Bob Sullivan. Bob Sullivan is The Perfect Scam.

You've got some great hosts on that podcast. I appreciate what they do. We'll make sure to link everything in the show notes, and thank you so much for coming on the podcast today.

Thanks for inviting me. I appreciate it.